UnitedHealthcare Health Insurance Review

Find out if UnitedHealthcare health insurance meets your needs.

Updated: May 22, 2022

Reviewed by: Tammy Burns

Insurance and health care consultant

Is UnitedHealthcare Good Health Insurance?

UnitedHealthcare offers numerous coverage options and rates well for customer service and financial stability.

Overall rating: 4.7

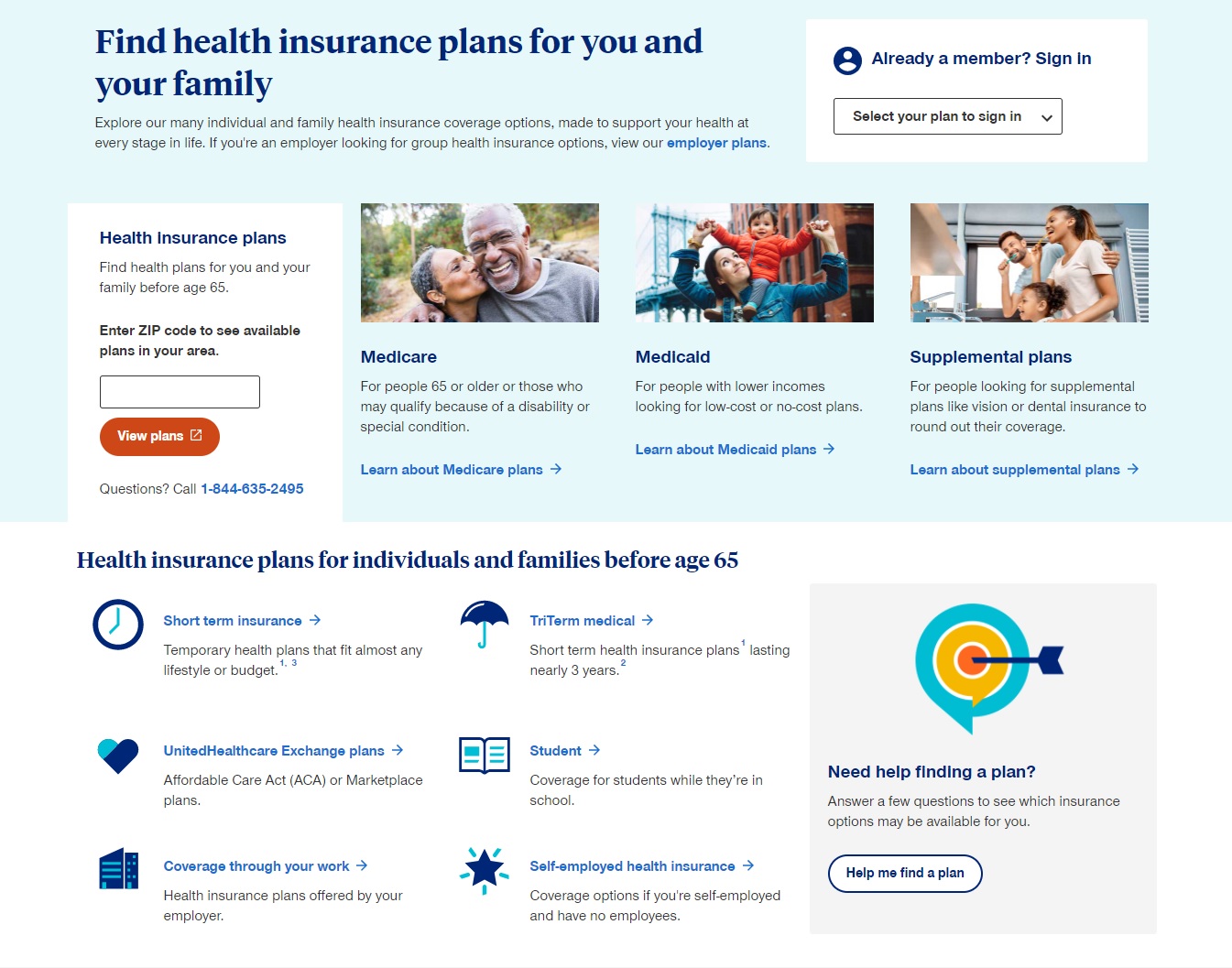

UnitedHealthcare is the largest health insurance company in the nation. Founded in 1977, this insurer sells policies in all states except New York. Among its policies are options for short-term health insurance, individual and family coverage, Medicare, vision, and dental insurance.

![]()

UnitedHealthcare Health Insurance Overview

| Company founded | 1977 |

| Coverage area | 49 states (excluding New York) |

| A.M. Best rating | A- |

| Better Business Bureau (BBB) rating | A+ |

| National Committee for Quality Assurance (NCQA) accreditation | Yes |

| NCQA rating | 4.5 to 2.5 |

| Plans available |

|

| Provider network |

|

Is UnitedHealthcare a Good Health Insurance Provider?

| What we like about UnitedHealthcare health insurance plans: | The drawbacks of UnitedHealthcare health insurance plans: |

|---|---|

|

|

What Do UnitedHealthcare Health Insurance Plans Cover?

- Dental

- Employer-based coverage

- Family

- Individual

- Medicaid

- Medicare

- Self-employed

- Short-term

- Student

- Supplemental such as accidental, critical illness, hospitalization, indemnity, and international travel

- Vision

UnitedHealthcare Health Insurance Plan Options

UnitedHealthcare has multiple plans across three metal tiers, letting you choose a plan with coverage that fits your needs. All of these plans are EPO plans. With an EPO, covered services are provided when you go to doctors, specialists, and hospitals in your plan’s network. Monthly premiums vary from $368 to $658, and most plans have maximum out-of-pocket limits of $8,500.

Compare some of UnitedHealthcare’s top health insurance plan options:

UnitedHealthcare Health Insurance Plan Options

| Plan name | Monthly premium | Annual deductible | Office visits | Annual maximum out-of-pocket cost |

|---|---|---|---|---|

| Balance Bronze 3 Free Visits | $367.99 | $7,500 per individual

$15,000 per family |

Primary doctor: 50% coinsurance after deductible

Specialist: 50% copay after deductible |

$8,550 per individual

$15,000 per family |

| Value Bronze Saver (HSA) | $380.13 | $5,900 per individual

$11,800 per family |

Primary doctor: 30% coinsurance after deductible

Specialist: 30% copay after deductible |

$7,000 per individual

$14,000 per family |

| Value Silver 3 Free Visits | $490.90 | $5,500 per individual

$11,000 per family |

Primary doctor: 35% coinsurance after deductible

Specialist: 35% copay after deductible |

$8,550 per individual

$17,100 per family |

| Balance Plus Silver 3 Free Visits | $493.47 | $4,500 per individual

$9,000 per family |

Primary doctor: $40 copay

Specialist: 50% coinsurance |

$8,500 per individual

$17,100 per family |

| Value Gold | $658.33 | $2,350 per individual

$4,700 per family |

Primary doctor: $20 copay

Specialist: $65 copay |

$8,500 per individual

$17,100 per family |

*Based on pricing for a nonsmoking 35-year-old female in Nashville, Tennessee.

How Is UnitedHealthcare Rated?

Trusted ratings and reviews can help you understand how an insurer’s plans stack up against the competition. See our UnitedHealthcare review.

Overall rating: 4.7

| Financial strength rating: 4 |

Customer satisfaction rating: 4.8 |

Value rating: 4.8 |

Coverage rating: 4.8 |

Financial strength: 4.5/5

UnitedHealthcare’s financial strength rating indicates how well it can fulfill its financial obligations to its policyholders. A.M. Best rates UnitedHealthcare’s coverage in each state individually, but no state earned less than an A-. Several ranked in the A+ category.

Customer satisfaction: 4.8/5

UnitedHealthcare’s customer satisfaction rating is based on BBB, NCQA, and Consumer Affairs ratings.

UnitedHealthcare has an A+ rating on BBB, indicating that it resolves customer issues with their plans effectively. In the last three years, 893 customer complaints have been closed.

UnitedHealthcare’s health insurance plans generally perform well, according to data gathered by the NCQA. Several plans are recognized as high-performing, and even those with the lowest scores are categorized as moderate-performing.

Consumer Affairs gives UnitedHealthcare a rating of 3.9 out of 5 stars. This rating is based on approximately 2,800 reviews.

Value: 4.8/5

UnitedHealthcare’s value rating is based on how much its plans cost compared against plans from other insurance companies. Factors influencing this rating include the monthly premium, coinsurance, copayments, annual deductibles, and out-of-pocket maximums.

Coverage: 4.8/5

UnitedHealthcare’s coverage rating reflects the types of coverage it provides. That includes options for individuals and families, older adults, individuals with limited incomes, and university students. The rating is also based on how many plan types are available and how easy it is to find an in-network health care provider.

Sources

- 091202UNITEDHEALTH _Rating Supplement_ | Last accessed June 2026

- BBB | UnitedHealthcare | Last accessed June 2026

- Consumer Affairs | United Health Care | Last accessed June 2026

- gov | Exclusive Provider Organization (EPO) Plan | Last accessed June 2026

- Insurance Information Institute: How to assess the financial strength of an insurance company | Last accessed June 2026

- NCQA | NCQA Health Insurance Plan Ratings 2019-2020 | Last accessed June 2026

- UnitedHealthcare | About us | Last accessed June 2026